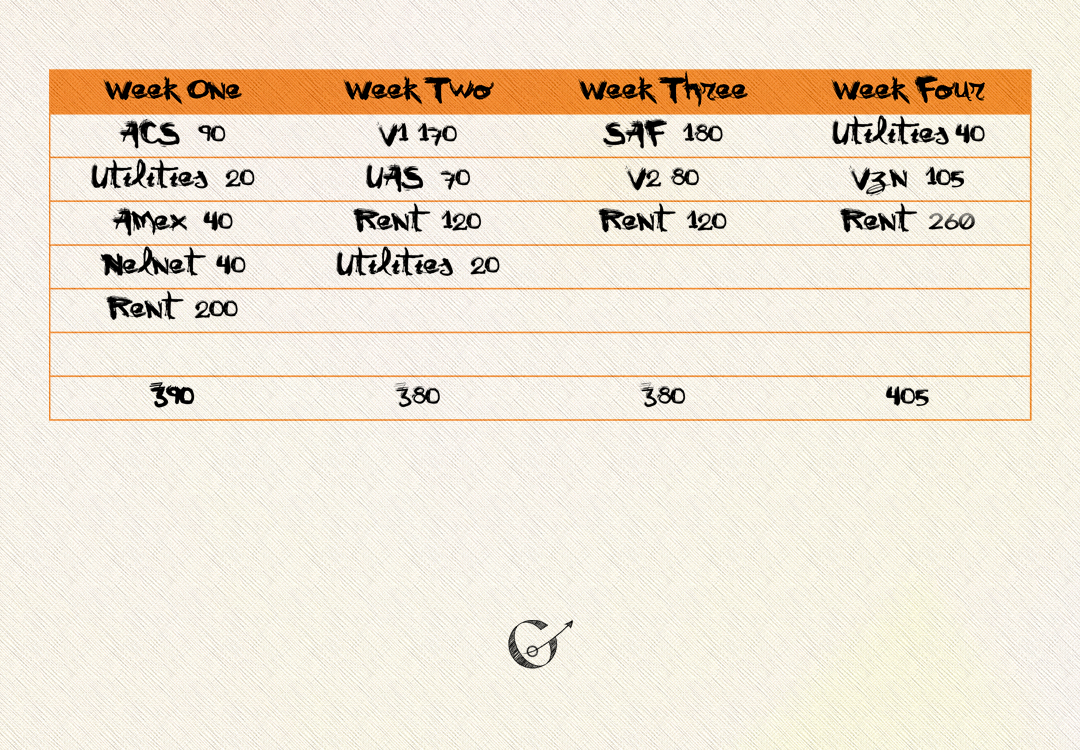

Budgets are like pokémon. They are great tools to help us through our journey and reach our goals. This four-part series takes a look at my budgeting history and my journey to finding my current budget. In part one, I shared my experiences of how my budgeting developed over the decade before moving to New York City. In part two, I shared the challenging battles from my first year living in New York City and my wins and losses. In part three, I shared my process for breeding my new budget. In part four, I count up through my budget’s biggest level-milestones as we have been training together. These milestones highlight the moments in my budget’s training when I noticed it become stronger or demonstrate its strength.  Level 1 Level 1 Level 1: Base Moves Training my budget began after it hatched. It was, and still is, set up in a chart with every column representing a week’s paycheck for that month. Each bill’s payments was assigned to a paycheck, usually the week before it is due. When I received that week’s paycheck, my budget directed that money to the predestined bill. Whatever money was not predestined, I could do whatever I wanted with! I started spending some time every Friday or Saturday morning directing money where it needed to go before spending any part of my weekly paycheck. I hung it up next to where I usually paid my bills and crossed of each bill as it was paid.  Level 4 Level 4 Level 4: New Move- Totals As with newly hatched pokèmon, it took some time to learn the basics of working with my new budget. For the first three months I used the exact same budget file and got used to directing my money each weekend where it was supposed to go. Then at level 4, it learned a new move, totals. I totaled up the payments for each paycheck and identified that the first week was bill heavy. Since my budget already had the ability bill split, splitting bills into smaller payments paid over several weeks each month, I used it to balance the totals. Totals defogged my sense of how much money was predestined for each paycheck and how much was left over.  Level 5 Level 5 Level 5: New Move- Additional Categories I started to learn how flexible my budget was when it grew to level 5 and learned how to add a new category. Food was the first new category added, since being hatched. I originally left out a category for groceries because I was trying to budget for known expenses. But by adding a category for food turned it into a known and predetermined expense. This new move came in handy over and over. When my fiancé and I decided to move in together, I was able to add a new category to save up for the move.  Level 8 Level 8 Level 8: Move Replacement- Anticipated Paycheck Like a replacing a piplup’s bubble with bubble beam, level 8 replaced totals with anticipated paychecks. Anticipated paycheck are standardized totals that did numerous things for my budget. First, it told me how much money I thought I needed to earn each week to pay my bills. Second, it told me how much money was predestined to go towards my bills. Third, it would add extra money towards certain bills, particularly debt, to keep the totals standard. Fourth, they provide me information so I know about how much money I need to make before I take a freelance design job.  Level 11 Level 11 Level 11: New Move Combo- Five-Paycheck Format As my budget continued to grow, I started to enjoy its sturdiness in directing money from my paychecks. I was so pleased that at level 11 it learned how to adapt to a five-paycheck format. Before level 11, the budgets only accommodated four paychecks a month. If there was a fifth paycheck, I chose to “use it wisely.” By creating a five-paycheck format, my budget used anticipated paycheck totals to plan the best way to use each paycheck and bill split the extra money in regards to my financial goals. It also adjusted the schedule of which payments went with which paychecks to keep payments on time.  Levels 18/19 Levels 18/19 Levels 18/19: New Applications of Old Skills Then at level 18 my budget demonstrated how adaptable to any situation it really was. I took a month-long design job in Florida from March to April. The job paid in three paychecks. I received one when I signed the contact, one when I arrived in Florida and one after the show opened. This job also took me away from my day job during that time, which meant I would not have my weekly paychecks. For a brief moment I flinched, but my budget was ready to rock polish and shine. It took the five-paycheck format and transformed it into a two-month format. My budget and I then used anticipated paycheck totals to figure out which weeks I would be getting paid from my day job and established those amounts. To figure out the Florida weeks anticipated paycheck totals was a little trickier. First, I determined that my paychecks from Florida would all go into savings first. Next, using the calendar for when I would receive each paycheck, I estimated how much money I would have and when. My budget then combined that information with the bare minimum payments needed for those weeks to establish anticipated paychecks for that time. Once the totals were established, I paid myself accordingly from savings each Friday, like I was receiving my usual weekly paycheck. During these weeks I did not receive any “extra” money. My budget shined brighter than a solar beam powered by harsh sunlight and solar power! Not only was it successful, but it worked with limited access to a computer, the internet, and without my bill books. Level 20: Hold Item- Words To Remember Just before level 20 I read a post at Budgets Are Sexy that was about focus punching towards the goal of financial independence. Shortly after my budget picked-up the phrase “Freedom>Money>Stuff” and has held onto it ever since. Level 24: New Move- Goals At level 24 my budget learned incorporating goals. Each week’s column had “recommendations” for how to spend any extra money. I found these to be nagging and off-putting. I saw the potential in the move and I’m glad I did!  Level 25 Level 25 Level 25: What!?!, My Budget Is Evolving Like an aipom learning double hit and then evolving into ambipom, learning goals caused my budget to evolve into its next stage at level 25. By evolving, my budget continued to grow stronger. The goals changed format, were labeled as goals and were separated from each weekly paycheck. Paired with its hold item, my goals were visible and encouraged me to reach for them. Level 32: Possible New Move- Credit Card Tracking Since level 25 my budget has landed many critical hits. However, my budget is frustrated that it cannot help more with my credit card relationship. It has tried numerous methods to lend a helping hand. At level 32 it started to attempt tracking interest (see Level 44) instead of giving a balance range for each month's statement (see Level 25). So far, this seems to have been the most helpful method, just not super effective. I think it has potential and am just waiting for it to bellossom.  Level 44 Level 44 Level 44: Move Replacement- Leftovers

For the last couple of months I have been testing a new move, leftovers. Leftovers is designed to forewarn me of how much of my bills are not accounted for with my payments. As of level 44, or May, I will have leftovers for both of my credit cards. To be clear, I am technically paying the minimum payment due. I use each credit card to pay a bill and then I pay that payment’s money to the credit card instead. That payment counts towards my minimum due using my money for the other bill. This is why I do not budget for the entire amount due. Sometimes in a pokémon’s training a very strong and powerful move needs to be forgotten for a short time because of an immediate need for another one. This is one of those times. Right now, I am in the middle of planning a wedding for August and work is in its slow season. My two main goals need to be paying my bills in full, without little tricks, and paying for my wedding. With level 44, my budget will forget goals for a little while and return once my life becomes a little more stable. My budget has gone through a lot of changes over these last few years. It has grown strong and I am glad to have such a sturdy pokémon being the base of my financial pokémon team. Although having a budget is important, I think having a budget that I work well with and works well with me is the most important quality to a budget. I have looked at other budgeting services like Mint, YNAB and Personal Capital, but I keep returning to this budget because it works the best for me. Let’s chat: There are more than 150 budgets out their just waiting to be discovered. Have you found yours? How does it work? Do you use a service like Mint or YNAB? Please share in the comments below. Who knows, your budget may be the budget that someone else has been looking for. Further reading: Best Free Budget Templates & Spreadsheets- Budgets Are Sexy You're not a useless piece of trubbish if you can't... budget- it's hard- From Rags to Reasonable

0 Comments

Leave a Reply. |

Bag Pockets

All

Blog

|

RSS Feed

RSS Feed

© 2016-2018 Tojo Designs/The Grown-Up Pkmn Trainer

Most images created for this blog are derivative works based on the copyrighted property trademarks, of The Pokemon Company Internationl, Inc. © 2018 Pokémon. © 1995-2018 Nintendo/Creatures Inc./GAME FREAK inc. Pokémon, Pokémon character names are trademarks of Nintendo.

Most images created for this blog are derivative works based on the copyrighted property trademarks, of The Pokemon Company Internationl, Inc. © 2018 Pokémon. © 1995-2018 Nintendo/Creatures Inc./GAME FREAK inc. Pokémon, Pokémon character names are trademarks of Nintendo.