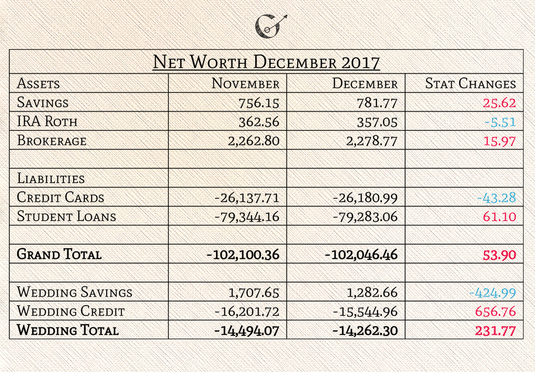

Welcome to January and 2018! The first post of the month means that it’s time for December's Review and Net Worth Update. For those who are new to The Grown-Up Pkmn Trainer, each month I write a financial review to xatu my net worth by writing down my thoughts on the previous and following months. I share these summaries so everyone can gain insight into my personal finances and my thoughts behind them. I started tracking my net worth to measure my progress, inspired by Budgets Are Sexy, which has helped me keep a keen eye on my personal finances. I have been tracking my net worth since January 2015 and writing monthly financial reviews for myself since 2016. I recommend both because they have been such helpful tools to watch my personal finances stat changes.  Summary of activity: December was a lovely month that went basically according to plan. We went to Montana for the holidays and were as busy as combee. We enjoyed seeing everybody and even got to meet my youngest sister’s two boys for the first time. I also encountered a math error in December's budget. Income Unusualness: I worked hard to stockpile enough hours to swallow for some missing vacation hours for my holiday trip. However, the final week in December still came up an hour short of my weekly 40 hours. I had no extra income this month. Overall Budget: My budget got a little messy in the middle when I didn't pay bills on holiday. That faked out my money a little and I had to quickly quiver dance once I got home to catch up. What really surprised me was when I realized that my budget's fourth week was $230 over budget. I’m thankful it could be easily reversed by just biding some time for the transfers to return the money. I don’t know what happened. I thought I checked those numbers at least twice. Errors happen, and at least now it’s been restored to full health.  Budget for January 2018 Budget for January 2018 Budget changes: January's budget has a considerable amount of changes for two reasons. The first is that I made it official that one of my goals for 2018 is to decrease my credit card debt by 5%. There is still some confusion about if I mean 5% of my current debt balance or my current debt limit. I have both numbers hanging next to my budget, so hopefully, I’ll hit at least one of them. The second is that since two of my student loans' amounts due greatly fell, thanks to the IBR, my husband and I discussed aiming some of that money towards our wedding line of credit. Using an online loan calculator, I determined reasonable payments for my credit cards and student loans that increase my credit card payments, lock-on money to our line of credit, while also lowering my student loan payments. I also checked everything 5 times to confirm my numbers for January. Net Worth: This month my student loans were the champion of the month by increasing my net worth the most. It was a five-week month, which may have helped. I anticipate about half of the holiday damage to appear in January’s update. Savings Accounts: My Ally savings is just hanging out eating leftovers. It didn't gain as much as was planned because my big credit card payment deposit didn’t go in before interest was added. It also was the excess budgeted money that didn't really exist. Way2Savings is basically sitting in the pc and not even running around the pelago. Investments: My Roth IRA, is still doing fine. In January I plan to either purchase new stock to diversify my portfolio (look at me sounding all grown-up) or beak blasting for February. I am really looking forward to it. My Acorns is currently giving me a market gain of 14.65%, with a total gain of 1.87%. I have been thinking about how I'm going to reallocate my portfolio in February. I may want to let it just keep doing its thing. Blackrock just keeps growing.  Credit Card PP Tracking Sheet for Jan.- April 2018 Credit Card PP Tracking Sheet for Jan.- April 2018 Credit Card Relationship: I went 1PP over on both cards, so hopefully I will remember next year to leave 6PP for December. As for the next four months, I have limited myself to 2PP for each card. If I want to reach my goal of lowering my credit card debt by 5%, I need to increase my payments and not spend as much, which I achieve by limiting my credit card usage.

Student Loans: The total went down, but my moody Nelnet rose sharply this month. At some point, I will give them a call to learn why the interest fluctuates so much. UAS and ACS balances continue to decrease. After all of my complaining about the reapplication process for my student loans as a married man, it resulted in harshly lower monthly amounts due. Instead of continuing to pay what I have been for these loans, my husband convinced me to aim some of that money to pay down our line of credit. Therefore, I am stance changing my meal plan for ACS by lowering its monthly payments. I used my loan calculator to adjust its monthly payments from being paid off by 2021, as I had originally intended, to being paid off around 2028. (Except my one loan that I have been overpaying for years and want to faint early.) As for Nelnet, I am suction cupping to my original plan of paying the minimum due until the others are paid off. It feels oddish, but the interest on the line of credit is double the interest from Nelnet’s loan's, and contributing to lowering our line of credit will be more rewarding to me. I understand that Nelnet may bring outrage and confusion, but I sadly can’t see any potential to pay them off in the next five to ten years like I do with my other loans. UAS is full steam ahead to be paid off by mid-2020. Wedding accounts: Our wedding accounts appear to have done very well this month because my husband forgot about bank priority moves. (More on that at the end of the month.) He scheduled a payment from wedding savings the same day the autopay was due to take the payment out of his checking account. Autopay has priority over account transfers, so the bank took the autopay out of his checking account before taking the scheduled payment from savings. Instead of using the $500 transfer as payment to stop the autopay, it credited the account with $800. It has since been resolved. I hope that by contributing $100 to our line of credit, I can slow it’s giga draining of our wedding savings. Once my husband learns what his student loans payments look like for 2018, he should be able to contribute more too. If we don't start contributing to the monthly payments, our wedding savings has about two months left. A side note; in my spare time, I figured out if I were to get an extra $10 an hour, over the course of a year I could pay off two-thirds of our line of credit with that extra money alone. Just fantasies for now… Other notes: After hanging with my sister's three boys and a wishwashi schooling of my cousins' kids, I can't want to wait to have kids. However, I honestly don't believe that we are financially stable enough yet. I want to lower my debts and increase my savings and investments this year. Then, maybe I'll be ready. If I don't improve my habits now, improving them with an extra mouth to feed will be like traveling through a rock tunnel without flash... sure, I can do it, but it’s hard to see and there is a lot of bumping into things. After a soothing plusle of a month, I am ready to take on January. Let’s chat: How were your finances in December? How are you preparing for 2018? Further reading: Rockstar Finances Blogdex Net Worth Tracker- over 475 other bloggers’ net worths November 2017 Review and Net Worth Update- last month’s review and update December 2016 Review and Net Worth Update- where I was a year ago *A few notes about my net worth* My net worth only tracks my personal assets and liabilities. My husband’s finances are not included. I include our wedding accounts on a separate line because I haven’t figured out how our accounts fit into my personal net worth. The numbers are taken from each accounts’ monthly statements. I don’t use dollar signs because looking at just the numbers helps me focus energy easier for analyzing by removing any prior attachments, emotional or otherwise, so I can look at the numbers as just numbers. (In my excel file, I don’t use commas either.) I only show the current month and the one before for illustrative purposes. (My excel file contains the entire year.) I use plusle-red, and minun-blue for illustrative purposes. (In my excel file, they are all in black.)

0 Comments

Leave a Reply. |

Bag Pockets

All

Blog

|

RSS Feed

RSS Feed

© 2016-2018 Tojo Designs/The Grown-Up Pkmn Trainer

Most images created for this blog are derivative works based on the copyrighted property trademarks, of The Pokemon Company Internationl, Inc. © 2018 Pokémon. © 1995-2018 Nintendo/Creatures Inc./GAME FREAK inc. Pokémon, Pokémon character names are trademarks of Nintendo.

Most images created for this blog are derivative works based on the copyrighted property trademarks, of The Pokemon Company Internationl, Inc. © 2018 Pokémon. © 1995-2018 Nintendo/Creatures Inc./GAME FREAK inc. Pokémon, Pokémon character names are trademarks of Nintendo.